This article originally appeared in the March 2015 edition of the ICAEW’s FS Focus magazine

Insurance has never been a particularly popular product to buy. People resent paying for something that they probably won’t need. They don’t like being boxed into products alongside average drivers when they believe themselves to be above-average even though statistics show we aren’t all excellent behind the wheel. People don’t like to feel fear, worny or a legal obligation forcing them to spend money on an 85-page policy document when they’d rather be putting it towards a brand new set of skis.

Against this backdrop in an increasingly transparent, customer-led and real-time world, insurance is an industry ready for change and one that is already adapting.

Many people believe that there are really only two types of customer shopping today:

- Transactional customers: these are focused on the things that are scarcer to them, heightening the importance of price, speed, and the effort required to purchase from company. They’re prepared to switch providers if a better offer appears;

- Relationship customers: they are keen to make sure they’ve made the best decision even if it takes a little longer, placing a high importance on the trust and confidence they have in the company and paying close attention to who their friends and family recommend.

For organisations to attract the latter, they need to be genuinely and consistently useful. Customer expectations of insurers are increasingly being set by their experiences with companies in other industries. This is inspiring change. Traditionally, the industry has focused on underwriting risk, helping to quickly deal with any losses and restore the customer back to the place they were in before, whether that be physically, financially or emotionally.

Increasingly, people are willing to share information about the way they live their lives in order to improve the quality of products and services they receive. Insurers therefore have an opportunity to refocus their businesses on the following areas:

- helping customers to understand the risks they face, challenging their inbuilt optimism bias and tendency to focus on the present rather than the future; and;

- reducing the risks and concerns that customers face, helping to keep them safe, healthy, or solvent.

Broadly speaking, there are three areas that insurers should consider for business opportunities in the future.

Serving data natives

Customers are becoming increasingly comfortable with their data, and they know what it’s worth to the companies that they deal with. Combining this with a world where people chase individualised products and experiences, challenging life-stage assumptions of how to live, the traditional insurance model of grouping similar individuals together and charging a similar price suddenly seems unsatisfactory – for both the customer, and for the insurers who could access a wealth of personalised data.

This is starting to lead to innovation. US-based Oscar insurance, for example, gives Bluetooth enabled fitness trackers to customers and rewards them with Amazon vouchers if they achieve 10,000 steps per day. Tech start-up Chargers rewards its app users for the C02 they save by travelling on a bike, bus or tram. App CompareMySpend allows people to share their financial data anonymously, so that in return they can see how similar people spend and save money. Users of the training app Strava in New York can opt to let the authorities see their cycling data, giving an unprecedented view of the most popular cycling routes in the city to focus safety improvements on the best areas.

By customers sharing this rich data, insurers have the opportunity to improve their risk-models, shifting to more individualised pricing and making the whole market more efficient, though there are fairness concerns should ‘too much’ individualisation serve to undermine the insurance business model. One drawback is that the necessary data still relies heavily on users opting. Studies also show the majority of owners stop wearing a fitness device within months of purchasing it.

Tapping into trust in networks

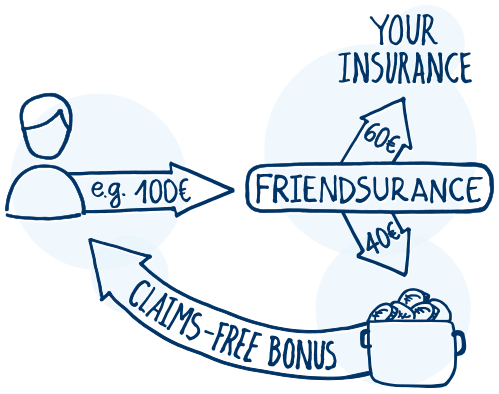

As insurers Guevara, FriendSurance and BoughtByMany demonstrate, social and peer-to-peer insurance is already here and likely to expand quickly. There’s an increasing belief that customers can cut out the unpopular, corporate, faceless middleman in favour of real people with similar lives and ambitions to themselves. The continued success of companies, such as Zopa for lending, TaskRabbit for odd jobs, and Airbnb for holidaying, show that the new wave of collaborative consumerism is more than a fad.

As this continues, an interesting tension is likely to emerge between those customers who are keen to have ultra-personalised product and pricing, taking the responsibility for themselves, and those who aren’t. Those in the second group are happy to combine into smaller groups of like-minded individuals, being aware that their behaviour will have consequences for the others.

This separation may prove to be one of the most interesting for the insurance industry to tackle in the coming years, satisfying both those who want the best price for themselves, and those who believe that working collectively is the preferred way – even if it means curbing their relevant excesses.

No time-wasting

The mobile world has dramatically changed how we spend our time. Customers expect to be able to do everything everywhere and when they provide instant information and feedback to companies they expect an instant response. Customers’ drive to have a life full of experiences means that those unexciting tasks have to be dispatched as soon as possible, allowing them to focus on what they deem to be most important.

App Google Now will look at your calendar, email, and search data, enabling it to give you the travel information relating to your next meeting before you’ve asked it the question. IFTTT (If This, Then That) is a web service that allows you to automate actions based on one simple statement, for example, sending a text message to your husband to tell him you’ll be home soon when your train reaches a certain station

And Tripcase aims to simplify your holiday planning, creating a detailed itinerary booking confirmation email. With everyone carrying a device that records location, can take photos, and scan documents, the insurance claims process should be easier than ever.

What’s clear is that people still don’t change as quickly as technology. The successful insurers of the future will therefore be the ones who embrace changes in customer behaviour and technology, by ensuring that they build an organisation that is customer-led with a clear purpose.

I really hope you enjoyed this article. If you did, I’d love you to subscribe to my blog at johnjsills.com/subscribe to get new thoughts sent to you on an infrequent basis, and find me on twitter @johnJsills.